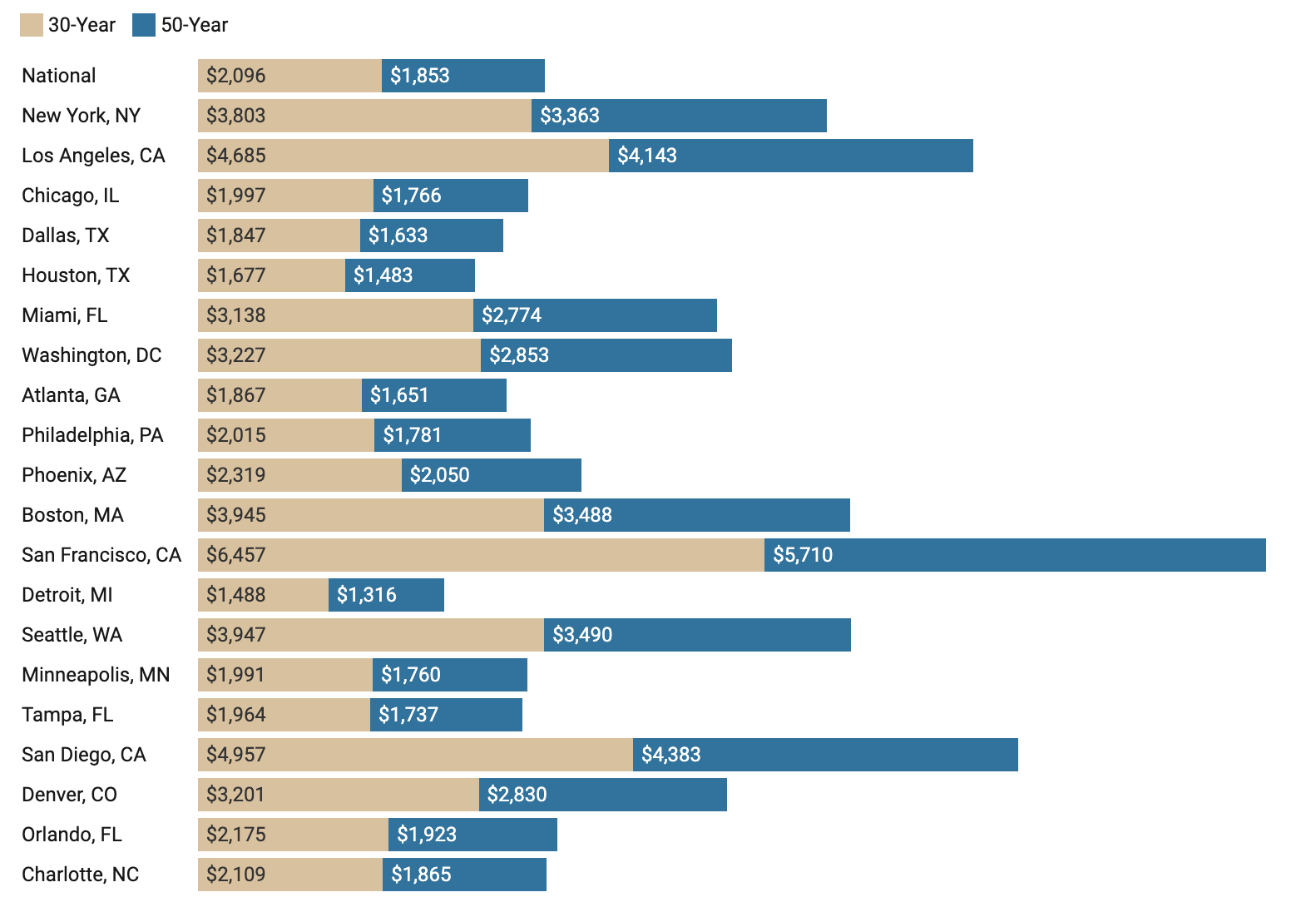

You’ll Save $2,000+ a Year with a 50-Year Mortgage

By far the largest benefit of a 50-year mortgage is that you’ll have lower monthly payments. For instance, if you bought a home at the national median home price of $426,800, your monthly payment would be $1,853. Choosing a 30-year mortgage increases the monthly payment by $200, resulting in an annual cost approximately $2,910 higher than a 50-year mortgage.

The annual savings are even more lucrative in California. If you bought a home for the San Franciscan median price of $1,315,000, your monthly payment with a 50-year mortgage would save you $8,967 a year over a 30-year mortgage. Similarly, in San Diego, you stand to save nearly $7,000 a year.

But there’s always a catch.

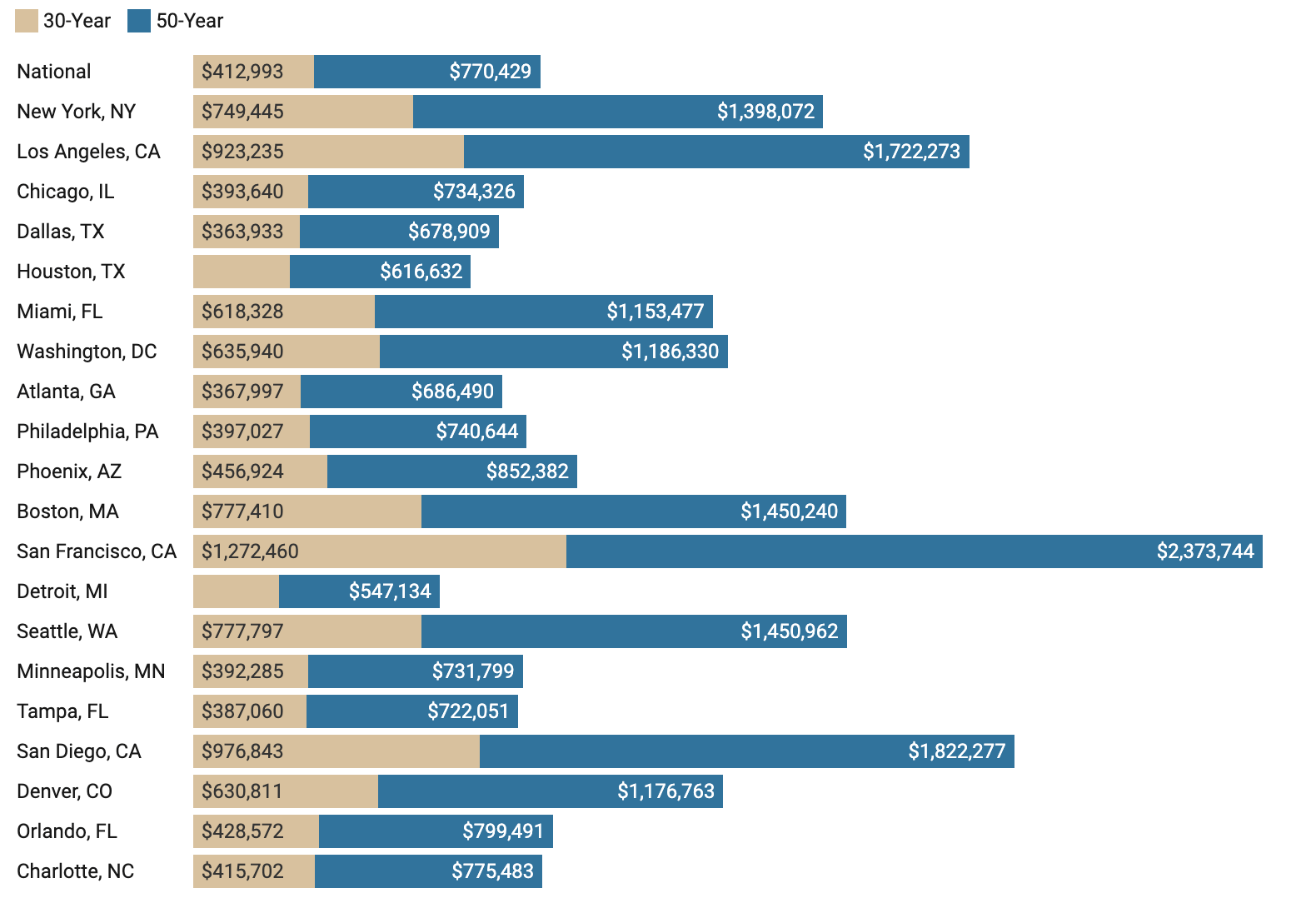

30-year vs. 50-year Mortgages: Difference in Total Interest Paid

Mortgages were calculated using the median single-family home price in each city and assuming a 6.22% fixed rate with a 20% down payment.

Are Double the Interest & Delayed Equity Worth it?

Initially, most of a borrower’s loan repayments are allocated to the interest, rather than reducing the principal balance. With a 30-year mortgage, it takes borrowers about 19 years before they begin paying more toward principal than interest (assuming a 6.22% interest rate).

A 50-year mortgage would significantly extend that timeline. Paying interest covers the cost of borrowing, but only payments toward principal reduce your debt and build equity. Not to mention that a 50-year mortgage comes with almost twice the interest.

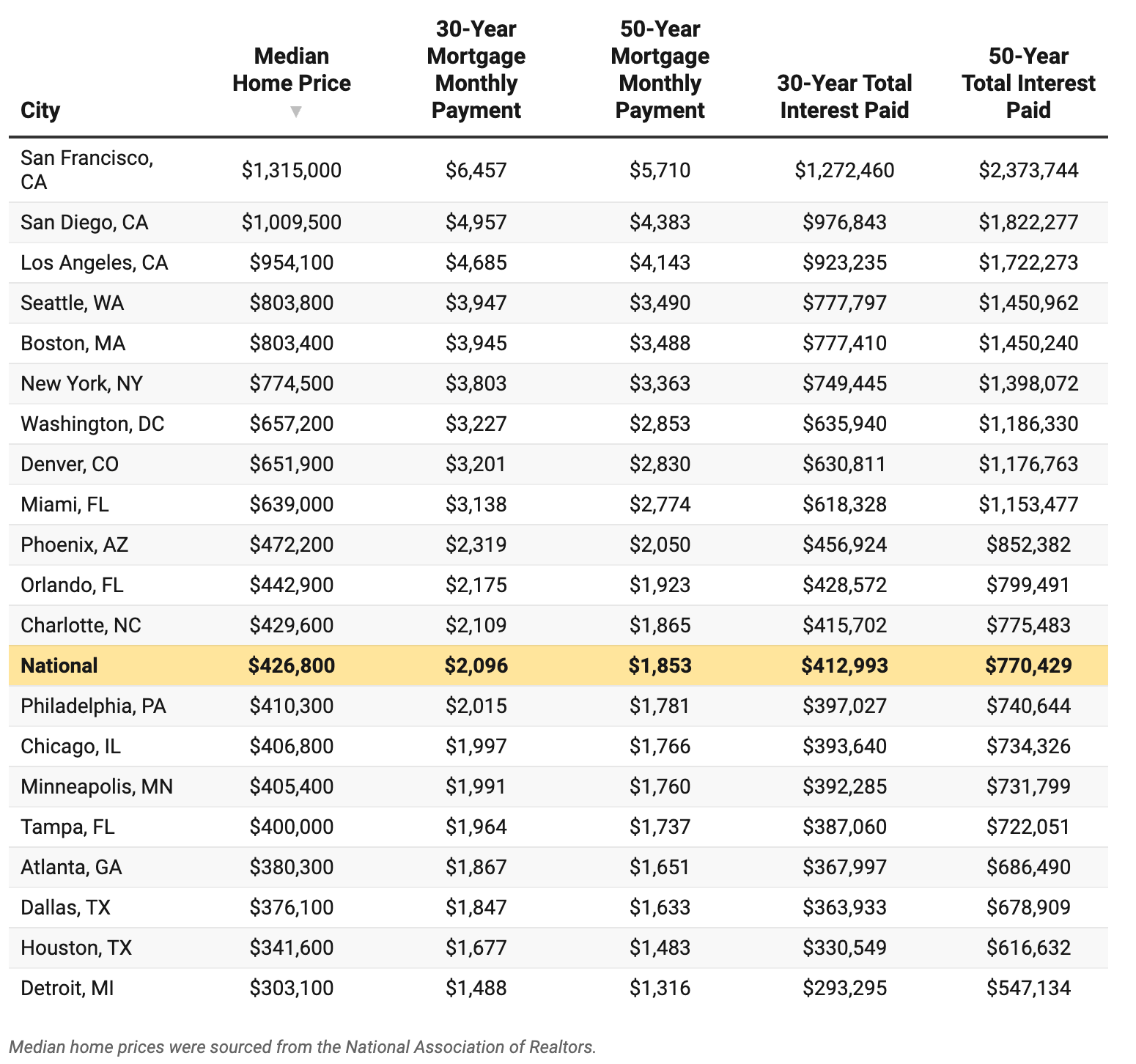

For a median-priced home in New York at $774,500, the interest a homeowner would pay with a 30-year mortgage is $749,445. With a 50-year mortgage, the total interest paid increases to $1.3 million.

Even in more affordable cities, the difference in interest paid on a 30-year mortgage and a 50-year mortgage is substantial. Take Detroit, for example, which has a median home price of $303,100. With a 30-year mortgage, a Detroit homeowner would pay $293,295 in interest, while a homeowner with a 50-year mortgage would pay $547,134. Opting for a 30-year mortgage would save that Detroit homeowner $250,000 in interest.

How Much You'll Pay in Interest on a 30-year Mortgage vs. a 50-year Mortgage

Mortgages were calculated using the median single-family home price in each city and assuming a 6.22% fixed rate with a 20% down payment.

But regardless of the mortgage length, the higher the home price, the larger the bill. One of the most effective ways for a homeowner to lower their mortgage bill is to purchase a more affordable home. The problem?

Many Americans don’t want to move outside their city to find an affordable home. A recent Zoocasa survey of over 1,000 respondents found that only 19% of Americans are willing to move to a different state to find a more affordable home. Meanwhile, over a quarter of respondents (31.6%) said they would only be willing to move within the same city, leaving little room for flexibility and potentially leading to overspending.

Down Payments Are Still a Big Hurdle

A 20% down payment on the national median price of $426,800 is $85,360. That’s 45.9% higher than the annual median wage of $58,500 for those aged 25-34 years old, according to the Bureau of Labor Statistics. Even 35-to-44-year-olds will struggle to come up with an average down payment, as their annual median wage is just $69,264.

With down payments exceeding annual wages, first-time buyers will need to scrimp and save for years before they can afford a median-priced home. This is likely a reason why the median age of first-time buyers has risen to 40—the highest it’s ever been. If that’s the case, then the typical buyer will be 90 years old by the time they finally pay off their home with a 50-year mortgage.

As a result, extending the mortgage term from 30 to 50 years will do little to help prospective young buyers save for a down payment. The entry point to homeownership requires financial stability that many young buyers don’t have.

There’s Just Not Enough Homes

In addition to down payment hurdles, home prices remain high. One reason is the severe lack of housing. A U.S. Chamber of Commerce report from September found that the country is short 4.7 million homes. When there aren’t enough homes to meet demand, then home prices increase.

Despite the need for more construction, housing starts fell in August. The most recent U.S. Census data shows that new residential construction decreased by 6% since 2024, while housing completions also fell by 8.4% last year.

In response, home prices remain elevated in most major markets. The National Association of Realtors’ latest median home price report shows that prices rose in 77% of metro markets. The Northeast experienced the largest price jump, up 6%, while only the West saw a price drop, down 0.1%.

Improving Housing Affordability Will Require Multiple Solutions

Longer mortgage terms will not drastically improve affordability for the average homebuyer. It may make monthly payments more manageable, but this comes at the expense of greater debt and delayed access to home equity. It also does nothing to address the barriers many prospective buyers face when saving for a down payment or securing a mortgage.

A multi-pronged effort is needed to address housing concerns. Americans need housing policies that support first-time buyers, increase construction, lower borrowing costs, and raise wages. Until then, the real estate market will remain inaccessible for many.

Are you thinking about buying a home this year? Start your search with US today!